Before I get into the guts of this post I want to make one clear distinction. I will be using the terms illiquid assets and illiquid investments interchangeably. This isn’t necessarily correct, so it’s worth noting. The topic deserves it’s own post, but for simplicity, investments are things you expect to increase in value (e.g. stocks), while assets are things that hold value (e.g. gold).

The trouble is that illiquid assets like gold can often appreciate in value. So are they investments or assets? I’m choosing to punt on this topic and warn you upfront that I will be treating them similarly throughout this post.

Now that’s out of the way, I’m going to go through several different asset types and talk about where they fall on the specturm of liquidity. After that we’re going to talk about why you should have more illiquid assets in your portfolio… something that seems opposite of conventional wisdom.

Understanding illiquid assets

To understand what makes an illiquid asset it’s easiest to start with what makes a liquid asset. Cash is the ultimate liquid asset because it’s money you can use today, right now. This can be hard currency cash, cash in your checking and savings account, or even cash in a money market account. As long as you have the ability to immediately access the funds, it’s considered cash.

Illiquid assets are just the opposite. They are things of value that are hard to convert to cash quickly and/or without losing a lot of value in the process. If you own a home, that’s a relatively illiquid asset. You can’t just decide to sell your house one day and have the cash in hand the next.

Other examples of liquid and illiquid assets

I’ve already mentioned cash and real estate, but where do these assets fall on the spectrum of liquidity? What other types of illiquid assets are there? What are their characteristics?

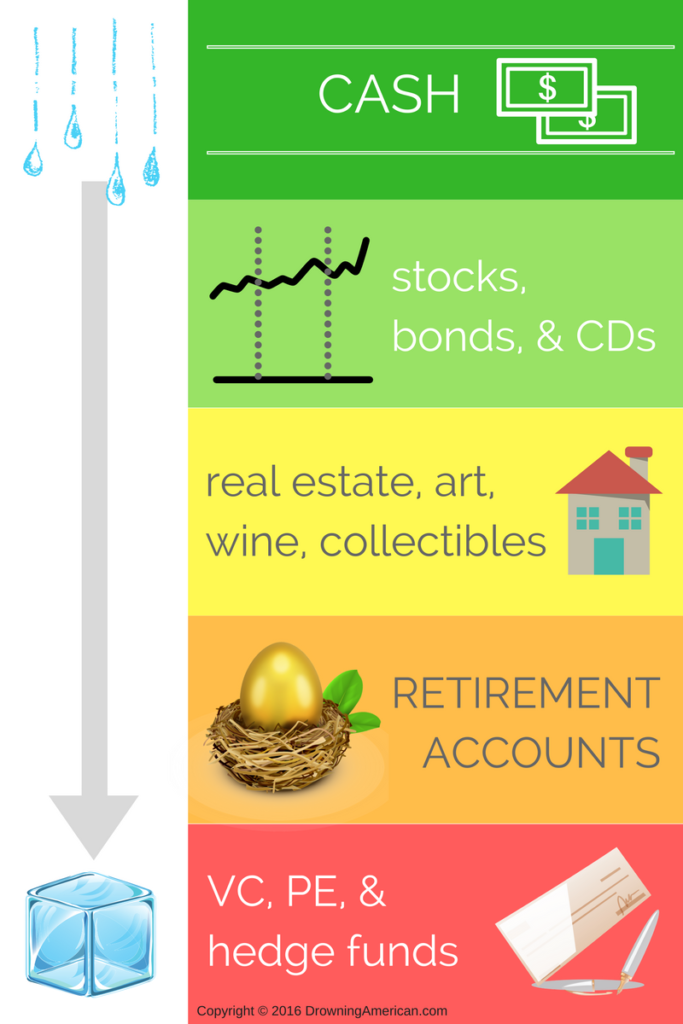

I made a graphic to help answer those questions. Let’s take a look at it and then go through each asset class:

Notice the graphic starts with the most liquid asset class, cash, and works its way down toward increasingly illiquid assets. We’ve already talked about cash and why it’s considered completely liquid. Let’s dive into the other asset classes.

Stocks, bonds, and CDs

I consider stocks, bonds, and CDs to be relatively liquid. Afterall, you can sell a stock or bond one day and usually have the funds in your bank account within a few days. The same goes for most CDs.

Some CDs may carry a small penalty for liquidating early, but it’s generally minimal. And if you need the cash in a crunch, it’s a small price to pay.

Real estate, art, wine, collectibles, etc.

We’ve already mentioned why real estate isn’t very liquid. It takes time to sell. The same can be said for illiquid assets like art, wine, collectibles, and other similar items.

You can’t simply sell a fine piece of art and have the cash in hand immediately… not without likely taking a huge hit on the value. You’d most likely take it to an appraiser and have it sold at auction.

That obviously takes time which means you’ll be waiting to turn that illiquid asset into liquid cash.

Retirement accounts

Moving down the spectrum of illiquid assets are retirement accounts. Although funds in retirement accounts can be accessed before you turn 59.5 years old, it generally can’t be done without taking a pretty hefty penalty. Remember, an asset is only liquid if you can turn it into cash quickly without losing substantial value.

Since retirement accounts are designed to be locked up until retirement age, these are largely illiquid. You have to wait quite a long time to access the money that’s accrued.

VC, PE, and hedge funds

Venture capital, private equity, and hedge fund investments are extremely illiquid. It’s rare that you can access your funds in these types of investments until there is a liquidity event. That means the company you invested in goes public or is acquired by another company.

I designate this the most illiquid asset class because you really have no control in accessing your capital in these investments. A retirement account can be liquidated, albeit with a penalty, but an investment in a private company cannot.

And this is the asset class that I strongly believe the average person should have more exposure to.

Why you should be investing in private companies

I’m a big advocate for putting your money in illiquid assets. If you have an employer 401k you should definitely be maxing it out every year. And while I could get into the advantages of doing so, that’s another post entirely. While many people own real estate (whether that’s their primary residence or rental properties), and many people have retirement accounts, not nearly as many people are investing in private companies.

There are two huge reasons why I believe more individuals should be investing in private companies. Let’s take a look at them.

Private companies are extremely illiquid assets

Sounds like a bad thing, right? It isn’t.

Think about your 401k. It’s relatively illiquid. It’s designed that way because we’re human; we’re susceptible to emotions and rash decisions. To protect us from doing something foolish with our retirement nest egg the government makes it pretty difficult to access our retirement accounts early. That’s because the longer your money is invested and untouched, the more time it has to compound and grow (generally speaking).

Another real danger is individual investors liquidating their stock and bond investments during a market crash. It happens over and over again and it is a huge destruction of wealth. I’m a big believer in locking up your investment capital in assets that are difficult to liquidate. Protect yourself against yourself!

Investing in private companies is a great way to lock your funds away in an investment that you can’t meddle with.

But what if I need that money?

For starters, I never advise someone to invest in private companies more than they can afford to lose. If you do that, by definition, you will never need this money.

But beyond that, there are few instances where you ever need to liquidate investments for emergency purpose. You should always have some cash on hand, and in this day and age there are a million ways to earn a living through the gig economy. When you fall on hard times, swallow your pride and find work. It’s out there. Don’t sacrifice the earning power of your investments.

Companies are staying private longer

The second reason I believe individual investors should be making bets on private companies is because companies are staying private much longer. Why is this a problem for you and me?

When companies hold off on going public we’re not able to invest early on. I bet you were using Facebook long before it went public in 2012 and would have loved to invest in a product that you use regularly and understand the value of. But you couldn’t.

When these companies finally do go public, they’ve already grown substantially. But it wasn’t always this way.

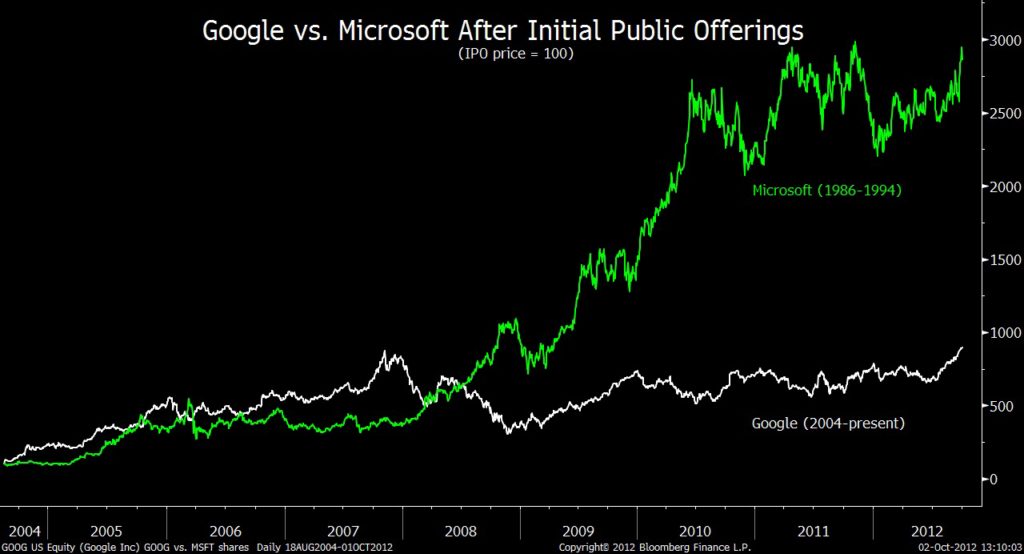

Take a look at this article from 2012 that discusses the first 10-year return of Google vs. Microsoft. Here’s the key chart from that article:

Basically, if you look at how each stock performed during their first ten years as a public company, you’ll see that Microsoft has drastically outperformed Google by that comparison.

In Google’s first ten years as a public company it increased in value by about 977%. That’s amazing… until you look at Microsoft.

In Microsoft’s first ten years as a public company it increased in value by 6,248%. Holy cow!!

The article I reference above makes this important statement:

“The key to long term IPO performance is initial valuation when going public.”

So if the initial valuation is already quite high, performance post-IPO is likely to be less lucrative. Again, all that means is that the longer companies stay private, the more big returns for investors are closed off to the general public.

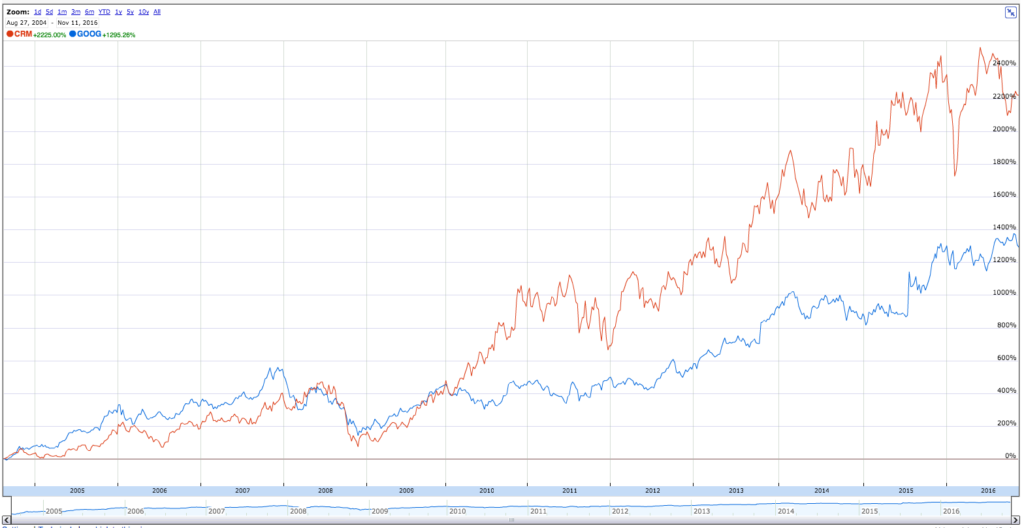

Here’s another chart comparing Google to Salesforce, a company that went public less than two months before Google:

Salesforce is up 2,225% while Google is up 1,295% in about the same time period. Salesforce’s market cap at IPO was about $400 million. Google’s market cap when it went public…$23 billion.

So what can we do?

The first thing you can do is ignore the hyped up companies that have realized a ton of value already as a private company. If Uber went public next year at it’s current $66 billion dollar valuation… would you be investing?

I wouldn’t.

I’m of the opinion there’s better value to be had by investing in companies that still have a lot of growth left and will do so as a public company. To put the Uber example in perspective, the company would be worth almost three times as much as Google when Google went public, assuming Uber is able to hold it’s valuation of $66 billion. I still prefer looking for companies like the next Salesforce, not the next Google or Uber.

Getting in pre-IPO

The other option, of course, is to invest before these companies even go public. But how do you do that? Isn’t it only for the wealthy?

Yes, and no…

I am not yet wealthy but I have made eight investments in private companies in the last eight months. The Internet and technology are increasingly democratizing the investment landscape. next month I’ll be covering my recent foray into angel investing and what I look for in the private companies I’ve invested in.